When we last wrote, some brave analyst at a Chinese brokerage was making headlines by talking of there being at least another CNY2–2.5 trillion in ‘shadow’ margin debt to add to the peak CNY2.3 trillion registered on the exchange ( that latter now already shrunken by over a third). Since then, the ante has been upped by one of our hero’s competitors, who added another CNY1-1.2 trillion to that already gargantuan guess. The man from Huatai Securities also suggested that half of the total was effectively being financed by the nation’s banks, whether they are strictly authorised to do so or not.

Who knows how accurate these estimates may be, but if, as is being bandied about everywhere, official margin at its peak represented no less than 9.5% of the free float value of the market, this would have put us up to a quota of around 25% at the peak of the mania.

NPLs, anyone? Bankrupt P2Ps? A big hit to corporate profits from the non-operating category? However it pans out, the charts show that technical support is not to be had anywhere soon – which only leaves a further embarrassing recourse to that suppression of market mechanisms which Xi and Li have spent their time in office disavowing.

With large percentages of stocks going either limit down or being suspended outright (around half of listed companies are presently to be found in the latter category) and with short-selling margin being increased to an eye-watering 30% in stock futures, the age-old, losing trader’s game of ‘pulling up the flowers and watering the weeds’ has taken on the dimensions of a wholesale deforestation, followed by a deliberate inundation. In short, those who cannot get out of their stocks, seem to be getting out of anything else they can sell in their place.

JUST GET ME OUT!

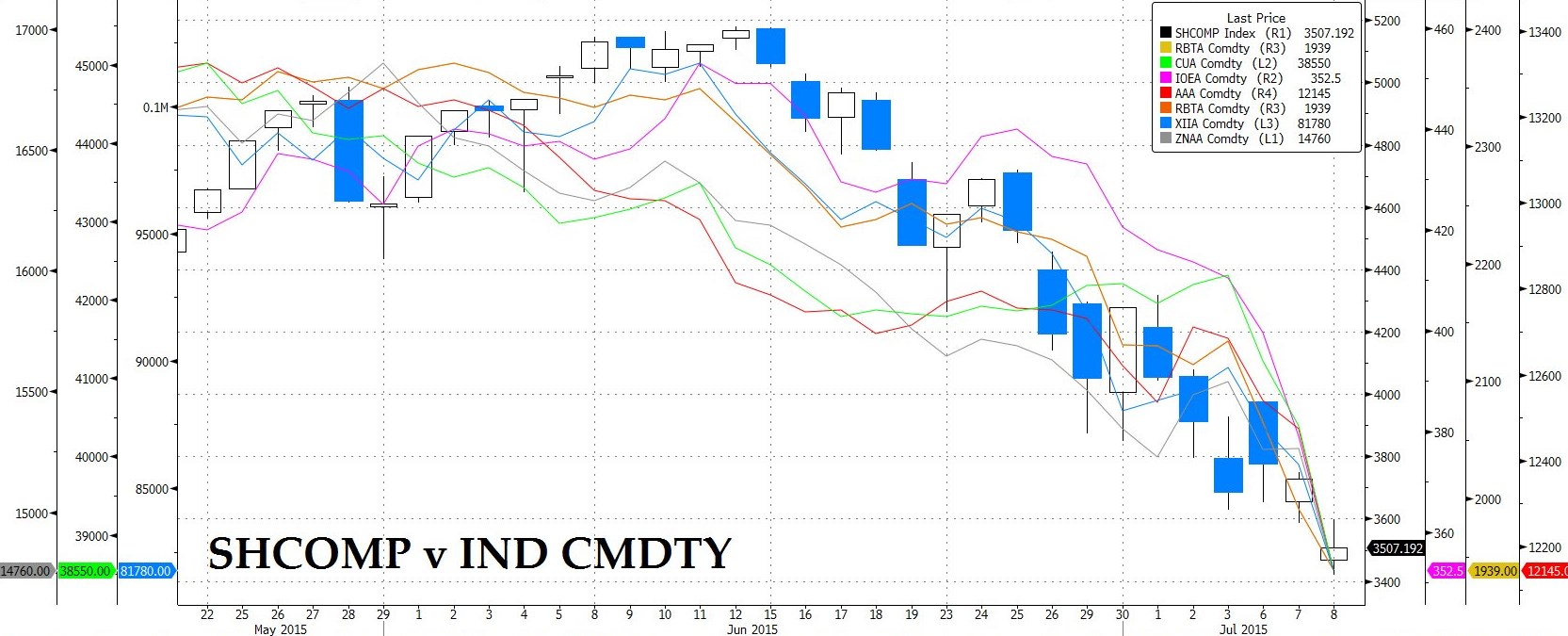

Courtesy: Bloomberg

Notably volumes have climbed dramatically on the commodities exchanges, even as prices have plummeted to new lows.The usual suspects—rebar, iron ore, copper, and so on—are all being caned along with the ChiNext. Whether any of these were being used for a little off-the-books financing play—this time to play the equity rather than the property market; whether it is a matter of liquidating to meet one’s broker’s demand for cash; or whether this is seen as a hedge against a wider economic/systemic melt-down is anyone’s guess. Short term oversold, yes: but the longer term bear market seems in remarkably fine fettle.

FOR A REGULAR INSTALMENT OF MY ANALYSIS, PLEASE VISIT ‘MONEY, MACRO & MARKETS’ AT HINDESIGHT LETTERS WHERE THE JUNE EDITION IS NOW AVAILABLE, AS IS THE LATEST WEEKLY ‘MIDWEEK MACRO MUSINGS’

NB The foregoing is for educative and entertainment purposes only. Nothing herein should be construed as constituting investment advice. All rights reserved. ©True Sinews