Amid all the debate about the US economy and the somewhat vague prospect of the Fed finally showing some cojones at some point in the future, the principle feature which allows the Doves to block any renormalization of the rate is the supposedly soft state of the labour market, particularly with reference to the sorry-looking participation rate.

It is bad enough that policy is therefore slave to a largely political, not a purely economic, factor, much less to an ill-defined, lagging datum such as this. On the one hand, the mighty NBER has belatedly lent its empirical weight behind the readily inferable explanation that this cycle’s unique package of extended unemployment benefits, coupled with a distinct loosening of the rules allowing one to declare oneself ‘disabled’ rather than out of work, has given us just about as much protracted idleness (OK – as much withholding of labour) as the state has been willing to pay for.

Add to this the difficulties being posed for the statisticians by the Uber/AirBnB generation, whose members are all presumably beavering away to pay off those college debts while awaiting their first VC visit by working far too informally and irregularly to be captured by a 1990s- style sampling methodology. This is a combination which, we could argue, makes for a jobs market that is much tighter than it appears – a contention that some private surveys are in fact starting to intimate.

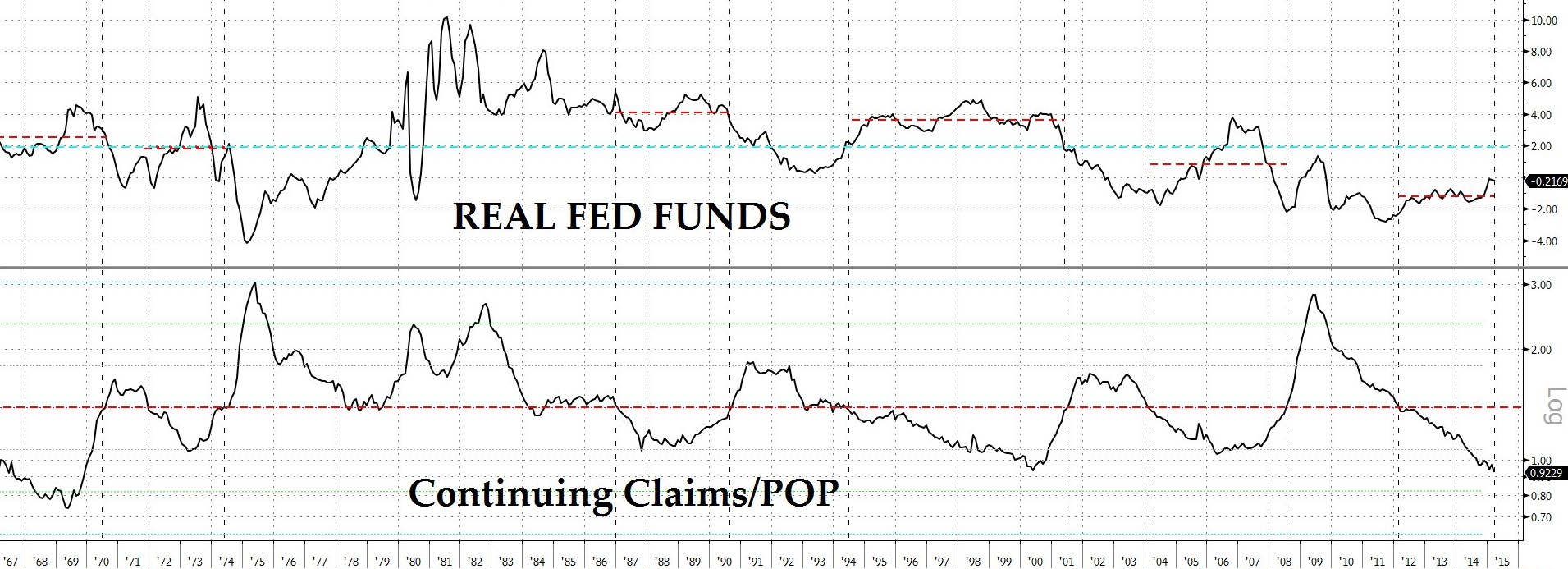

Even without going too far into such realms of speculation, we can see that the good, old initial claims data is screaming that the Fed is so far behind the curve that, floored throttle and all, it may be about to shoot right up over the top of the banking and into the Budweiser tent.

NO-ONE LEFT TO HIRE? REAL FF v CONT CLAIMS/POP Courtesy Bloomberg

Over the last 50 years, real Fed funds have averaged +2.0% but in the half of that stretch when continuing unemployment claims were lower than their particular average, the funds rate’s own mean shifted higher to 2.6%. The past four years’ mean? Minus 1.2%! And that with the claims count at a 46-year proportional low and a 15-year outright one.

The one caveat we would issue here – one which we will deal with at greater length in our next commentary – is that the wage bill is currently outstripping revenues (especially in the extractive and non-durable goods sectors, of course) in a manner which often tends to an increase in unemployment. The question here then is whether profits per payroll dollar can be maintained as sales per payroll dollar fall.

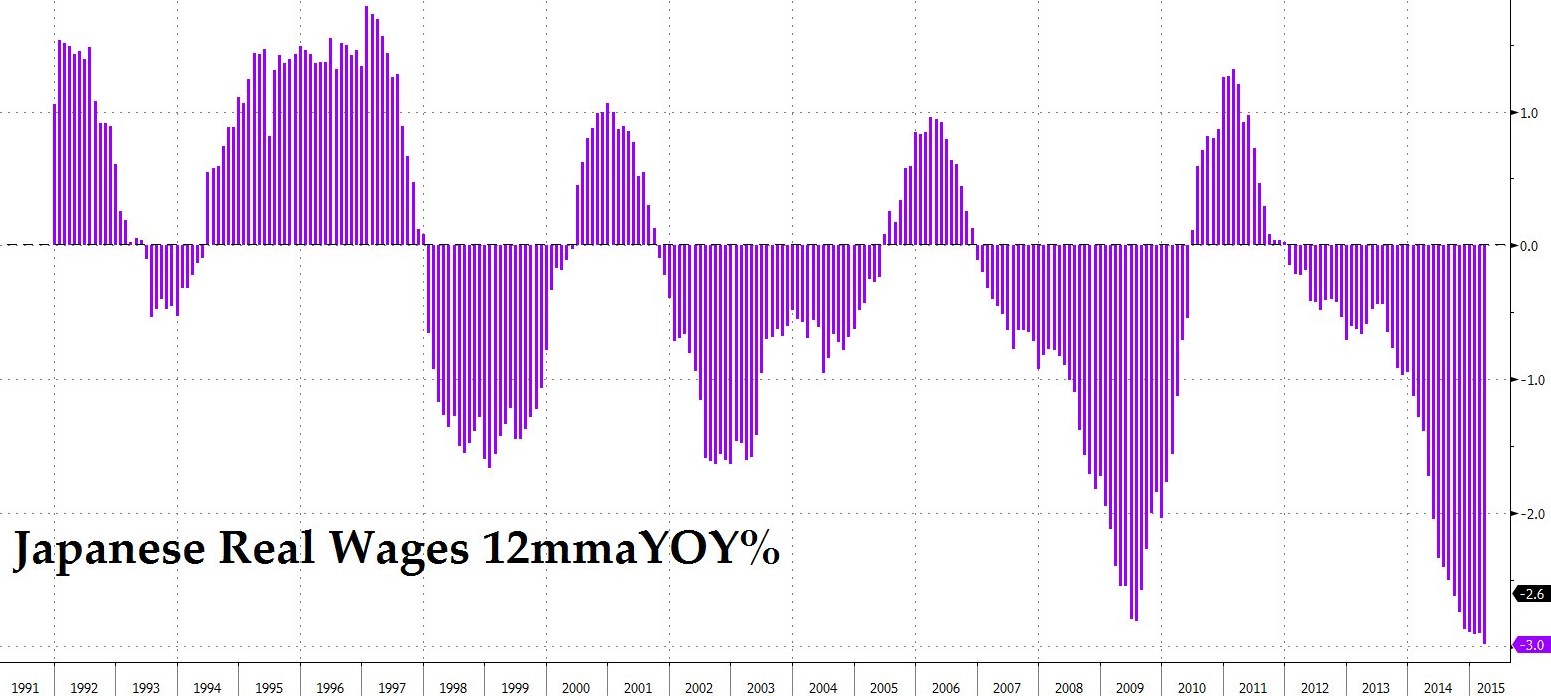

Over in Japan, we suspect that people would be ready to swap their sorry lot for that of people in a country where employment is expanding and real wages are rising. Not so in the Land of the Sinking Yen, thanks to the risible hodge-podge of Rooseveltian egg-o-nomics foisted upon their unfortunate populace by Abe and Kuroda. Real wages there continue to decline in a manner not yet being countered by overmuch extra hiring.

No relief can be in sight while a mindset persists of the type that can give rise to the comments made last week (when the monthly CPI shrugged off a spell of five months out of six spent in the negative column with a sudden surge to a 10-month high) by someone who really should have known better: viz., ‘Japan narrowly avoided deflation this month‘.

What he should have said, of course, was that ‘Japanese workers and pensioners were again narrowly denied a rise in their standard of living.’

JAPANESE REAL WAGES UNDER ABENOMICS Courtesy Bloomberg

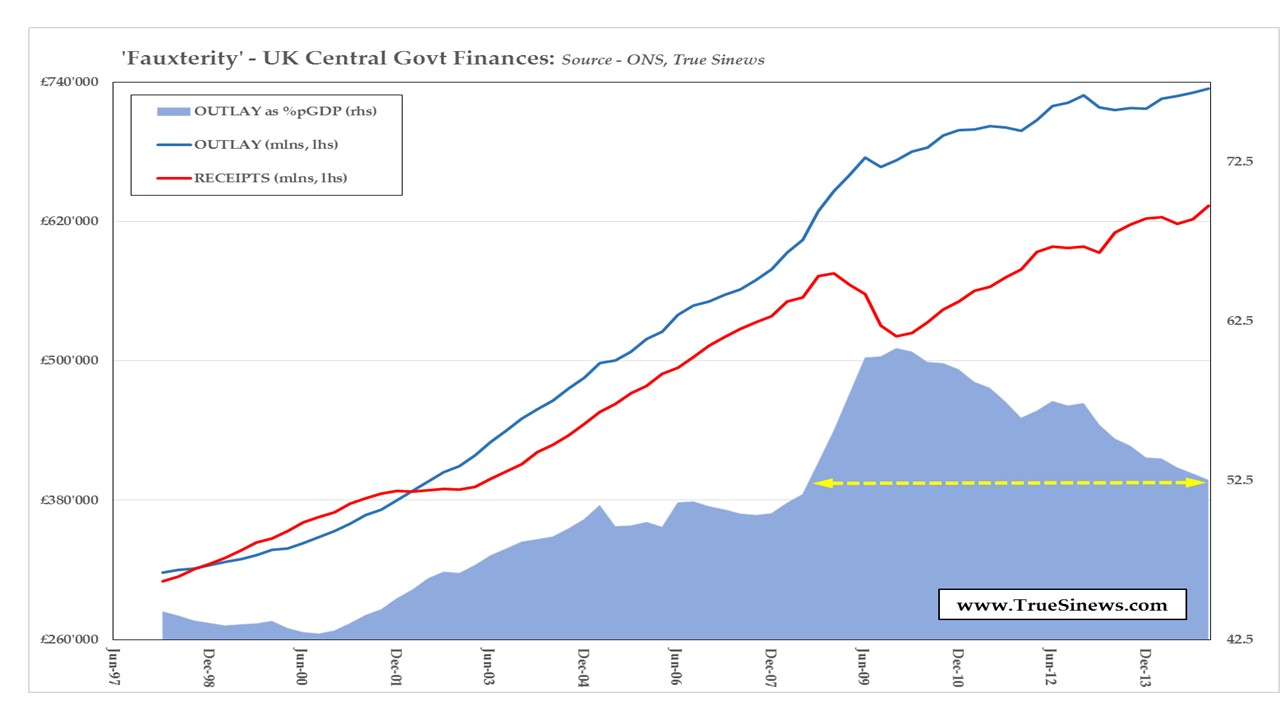

Now, ahead of Thursday’s UK general election – you know, the one in which a confusing cluster of red, purple, green, and Welsh socialists may just gang together to beat out the mainly English parties which stand slightly to what is known as the ‘right’ of them – here’s a trick question. Define the swingeing ‘austerity’ which that unsurpassable stand-up comedy act, Paul Krugman, recently used to test the tensile strength of the veins in his forehead in the form of the full blown rant he unleashed against its supposed practitioners in the op-ed pages of the British progressives’ organ of choice, the Grauniad (sic)?

OK. So would it include an expenditure total still setting new records? One in which £1 in every $7 spent was still having to be borrowed (largely from the ill-informed refugees fleeing Mario’s policy of mass rentiercide)? One where spending as a proportion of non-government GDP was still above Culpability Broon’s economy-wrecking heights of pre-Crash profligacy? Or one where that same proportion was fully 10 percentage points above that of the previous cyclical golden age, way back in 1997 when the first Blair government had not yet had time to realise its D-Nightmare programme of ensuring that ‘Things Could Only Get Worse’?

UK ‘FAUXTERITY’ IN ACTION: SLOWER INCREASES, MORE TAXES, NO CUTBACKS Courtesy Bloomberg

No? Well then, just take a glance at the above chart and tell us if the ‘austerity’ debate is anything more than a sham.

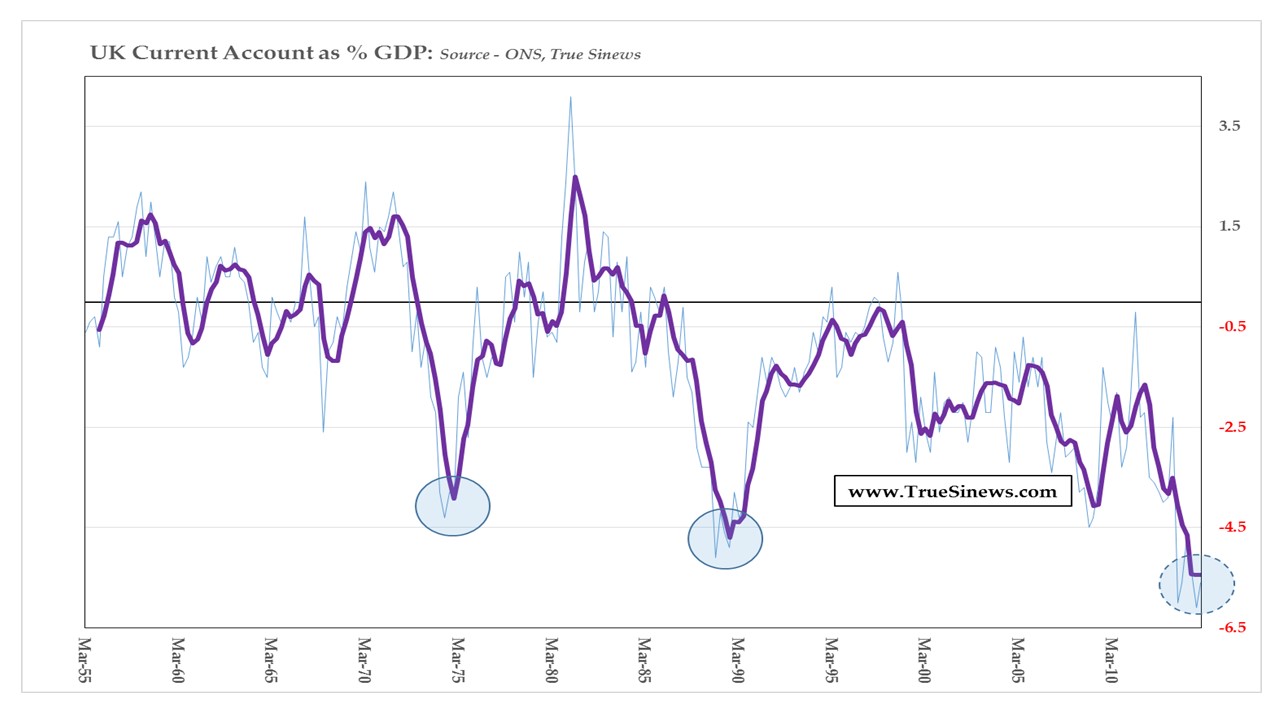

But if it is a sham, it’s a dangerous one, for the supporting monetary laxity entrained by Mark Karney’s Circus is beginning to turn potential evil into actual harm. Whereas, in the wake of the traumas of 2007-8, corporates and households alike were rebuilding their finances by setting aside around £7o billion annually and so were largely offsetting the state’s gross intemperance, today the former are saving nothing while the latter ended 2014 running up the biggest tab since the heady days when Lehman’s doors were still open and Chuck Prince was dancing the Charleston over at Citibank.

That then only leaves Johnny Foreigner to pick up the tab and luckily he is presently keen on the assets of a country where there appears to be some semblance of growth and where interest rates have critically not turned into warehouse dues across much of the yield curve. The terrifying scale of the UK’s reliance on his enthusiasm can be seen from its flipside in the yawning, all-time record current account gap being posted.

UK CURRENT ACCOUNT: THE KINDNESS OF (NIRP-AFFLICTED) STRANGERS

Given this, who would be sterling bull? Who, with the politics of coalition so untested in the land? Who, when the grim possibility exists of a minority administration being lashed to the wheel by the Fixed-Term Parliaments Act, there to be supported and hectored by a group of Gaelic extortionists, all eager to bury the ignominy of their referendum defeat ‘neath a cromlech of Sassenach tax monies.

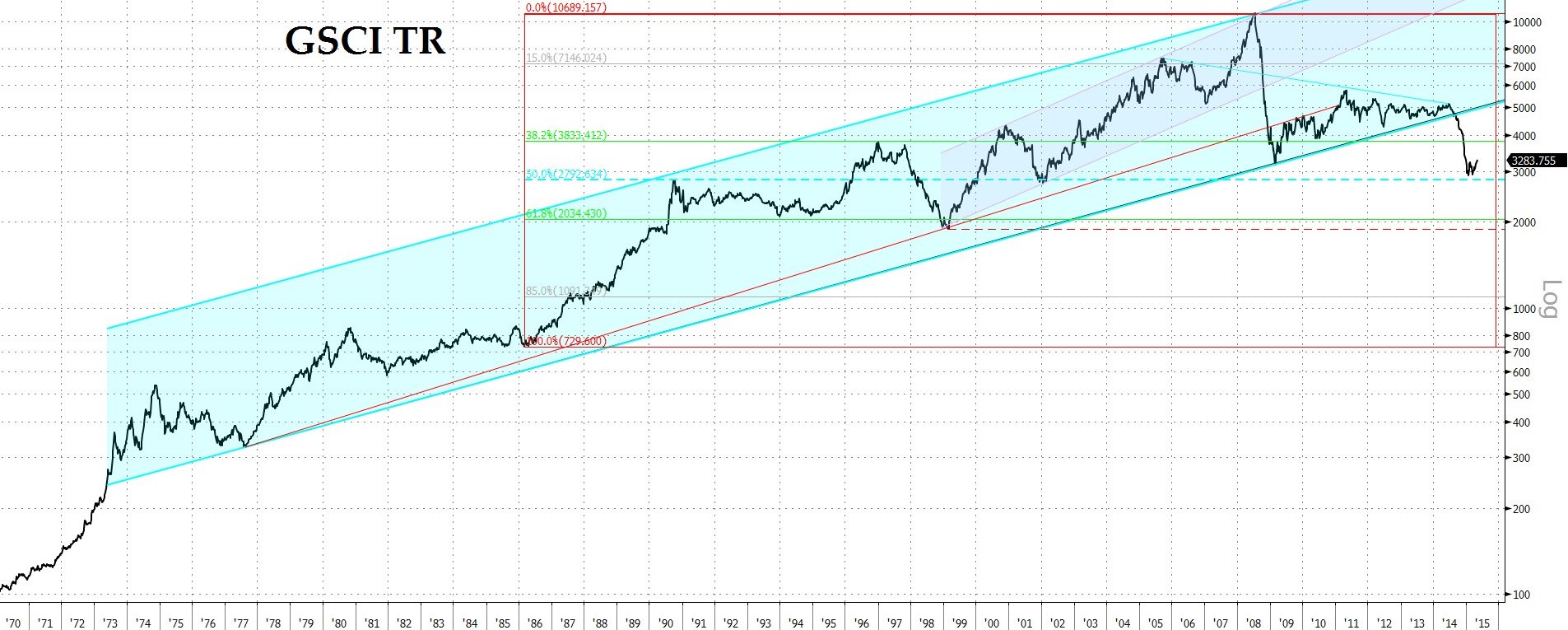

Outside of macro, we are just starting to shake off a little of our long-term dislike for commodities (even if we still believe in that repeated triumph of human adaptation and skill over human cupidity which tends to make them ever cheaper in real terms as the ages pass). Or, rather, let us rephrase that: we are beginning to think that conditions may be ripe for the blossoming of one of the market’s ‘Fair is foul, and foul is fair’ shifts of preference, hence why commodities have at last managed to find some tentative support after their long, long fall from grace.

BEGINNING TO BALANCE: DONE WITH DIVE-BOMBING? Courtesy Bloomberg

Against stocks, the pattern of relative returns is almost too perfect to ignore and here one should remember that during the ratio’s larger episodes of reversal it is usually stock weakness, rather than any untoward commodity strength, that marks the beginning of the move.

WAITING FOR A CLEAR PEAK REJECTION TO GET ABOARD A REVERSAL Courtesy Bloomberg

Against bonds, too, we have the classic negative correlation between a class of instruments which tend not to like too much growth or very much price inflation and the very things which the first most rapidly chews up and in which the second manifests itself much more vigorously than in just about any other entity else.

THE WARP AND WOOF OF WORLD MARKETS Courtesy Bloomberg

Doubts have already arisen regarding the sanity of owning bonds, even if mass central bank intervention makes shorting – rather than simply avoiding – them a trifle Quixotic for now. Nevertheless, with returns as far out of kilter as they are, it is hard not to be tempted by a little mean reversion play, just to break the monotony.

NB The foregoing is for educative and entertainment purposes only. Nothing herein should be construed as constituting investment advice. All rights reserved. ©True Sinews